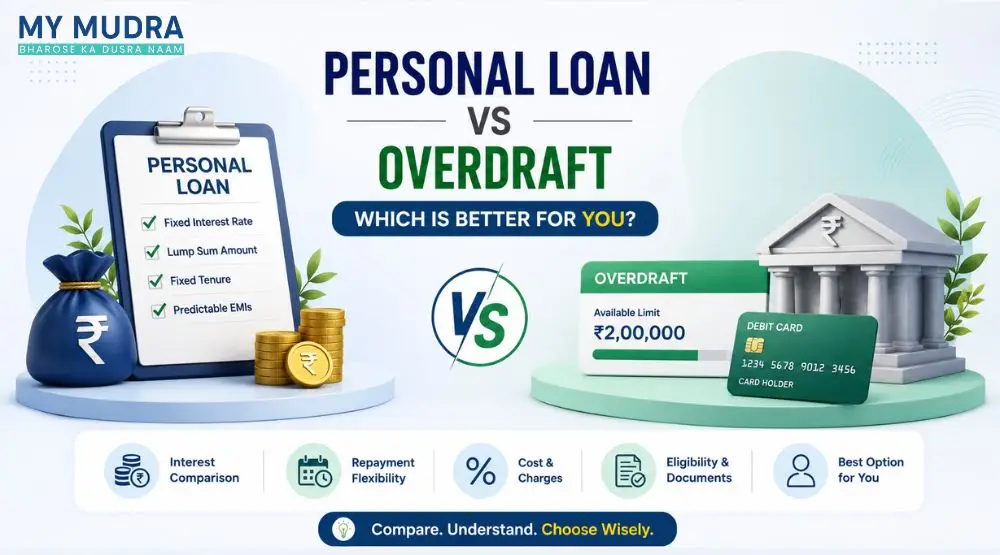

Personal Loan vs Overdraft: Which is Better for You?

Confused between a Personal Loan and an Overdraft facility? Explore the key differences, benefits, repayment flexibility, interest rates, and eligibility criteria to choose the right borrowing option for your financial needs in 2026.

Anjali Singh

Assistant Manager

May 20, 2026