Flot Loan App Review 2026 — Safe or Scam? + Better Alternatives

A complete review of the Flot Loan App covering safety, RBI approval status, features, and whether it is reliable for borrowers in India.

Anjali Singh

Assistant Manager

Apr 2, 2026

A complete review of the Flot Loan App covering safety, RBI approval status, features, and whether it is reliable for borrowers in India.

Anjali Singh

Assistant Manager

Assistant Manager

Hey there, I'm Anjali Singh. With over 6 years of experience in finance, I specialize in creating content on banking, loans, and financial planning. My goal is to simplify complex financial topics and help readers make informed decisions through my articles.

Others · Jun 20, 2026

IVF treatments and maternity care can be expensive. Learn how pregnancy loans and IVF loans in India can help cover fertility treatment, hospital expenses, delivery costs, and related medical needs with affordable repayment options.

Others · Jun 16, 2026

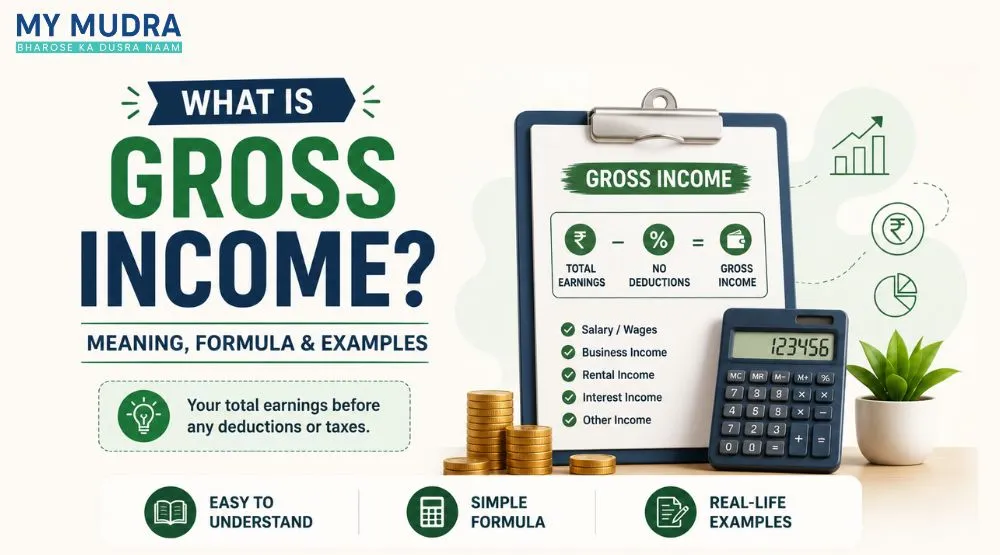

Gross income is one of the most important financial terms used in salaries, taxation, and loan eligibility. Learn its meaning, formula, calculation method, and practical examples to better understand your financial position.

Others · Jun 13, 2026

Planning to open or expand a multi-chair dental clinic? Learn about dentist practice loans in India, including eligibility criteria, interest rates, required documents, loan amounts, and financing options available in 2026.