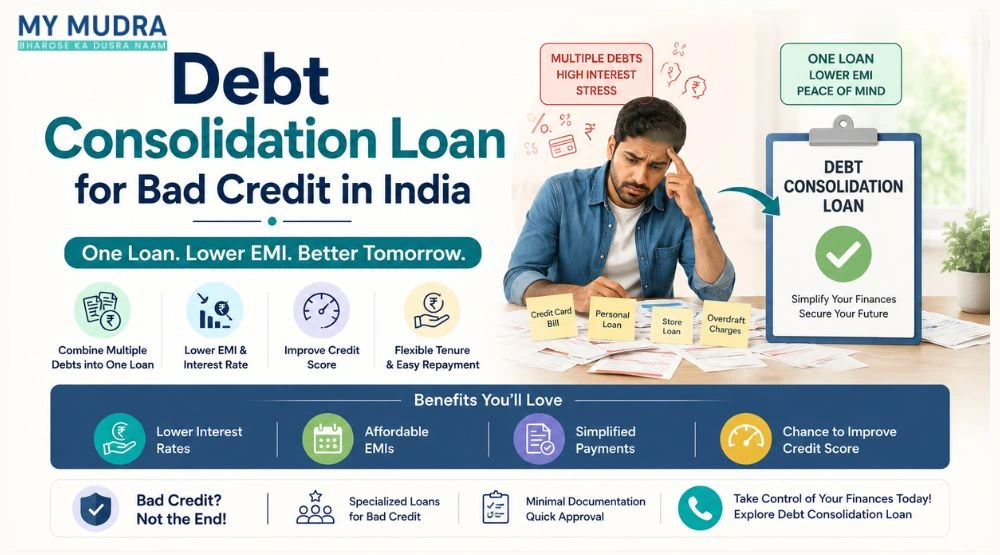

Debt Consolidation Loan for Bad Credit in India

Managing multiple debts with a low credit score? Explore debt consolidation loan options for bad credit borrowers in India and learn how to improve approval chances.

Anjali Singh

Assistant Manager

May 16, 2026