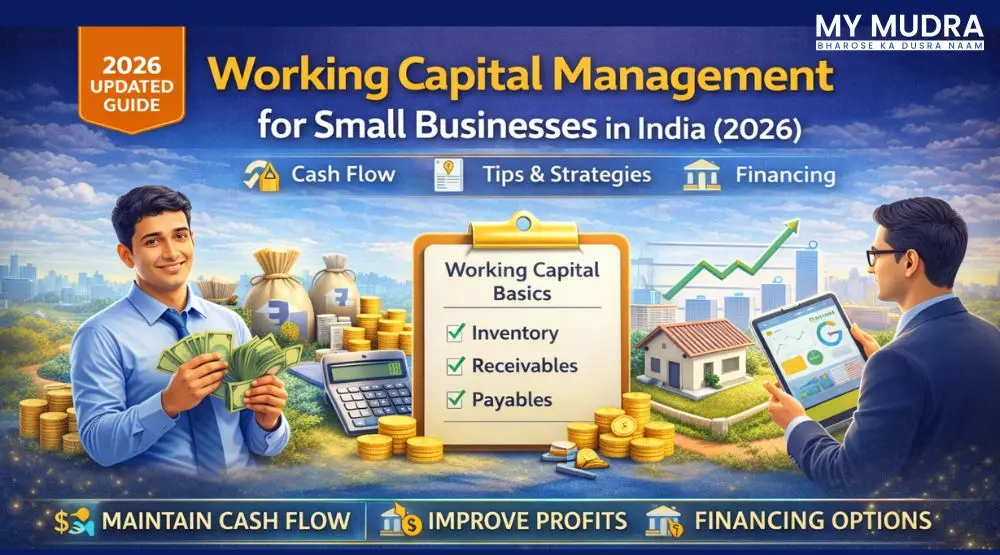

Working Capital Management for Small Businesses in India (2026)

Effective working capital management is crucial for small businesses to maintain smooth operations and growth. Learn how to manage working capital in India, improve cash flow, reduce financial risks, and build a sustainable business in 2026.

Anjali Singh

Assistant Manager

Mar 30, 2026

Frequently Asked Questions

Anjali Singh

Assistant Manager

Hey there, I'm Anjali Singh. With over 6 years of experience in finance, I specialize in creating content on banking, loans, and financial planning. My goal is to simplify complex financial topics and help readers make informed decisions through my articles.