Short-Term Debt Mutual Funds: Returns, Risks & Best Options

A simple guide on short term debt mutual funds work, their returns, risks, taxation & who should invest for stable income in India.

Rajat Kulshrestha

Head of Mutual Fund Distribution

A simple guide on short term debt mutual funds work, their returns, risks, taxation & who should invest for stable income in India.

Rajat Kulshrestha

Head of Mutual Fund Distribution

Head of Mutual Fund Distribution

Rajat Kulshrestha brings over seven years of experience in public markets, specialising in fundamental analysis and valuation frameworks. In his role as Mutual Fund Distribution Head, he oversees portfolio strategy, asset allocation decisions, and fund evaluation processes. On this blog, he offers structured, research-oriented perspectives on SME-listed companies, aiming to enhance financial literacy and analytical depth among market participants.

Mutual Fund · Jul 1, 2026

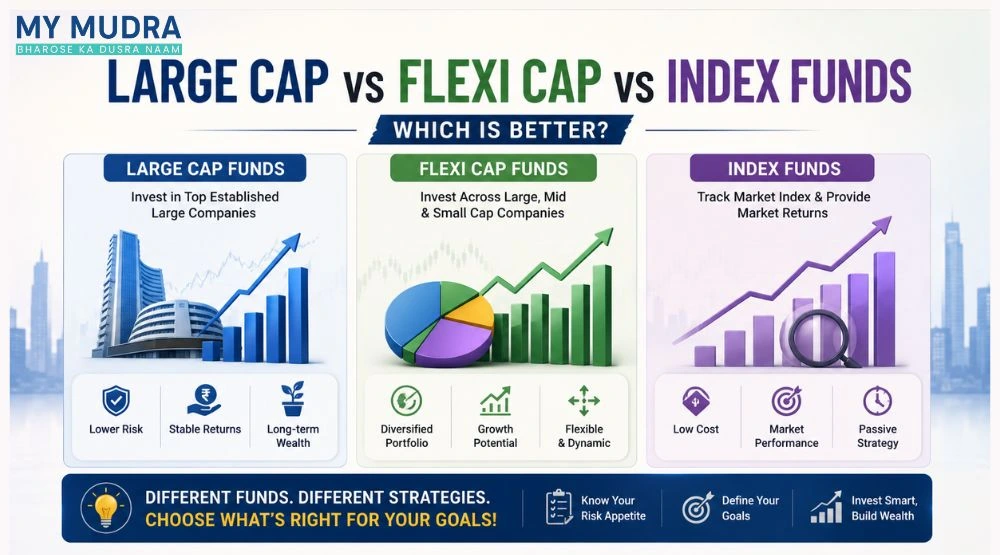

Simple guide to large cap, flexi cap and index funds. Compare risks, returns, costs and find the best mutual fund for your financial goals easily.

Mutual Fund · Jun 29, 2026

Understand why market crashes happen, how SIPs respond to falling markets, and the importance of staying invested for the long run.

Mutual Fund · Jun 11, 2026

Want to start investing with just ₹1,000 per month? Explore the best SIP plans for beginners in 2026, compare mutual funds, expected returns, risk levels, and investment benefits.